Self-Directed TFSAs: The Ultimate Guide for the Canadian Investor (2022 Update)

Canada has a comprehensive taxation system and it would be a rare exception that a transaction can skip its tax net. The whole tax system is designed to promote tax collection and, in turn, fulfills the society’s infrastructural, developmental, and economic needs.

A taxation system also provides an opportunity for a government to improve its image by introducing savings and retirement schemes benefitting residents. The Canadian government introduced the TFSA (Tax-Free Savings Account) in 2009 as one such option for its residents of 18 years or older with a valid Social Insurance Number (SIN).

You can keep a TFSA to park your savings and earn interest in a tax-advantaged environment. Alternatively, make it a more robust self-directed TFSA and invest in shares, bonds, GIC (Guaranteed Investment Certificates), mutual funds, gold and silver bullion, and others. This way you can create and manage a portfolio by using your tactics, investment strategies, and risk appetite. The beauty of a self-directed TFSA is that it is suitable for a person of any age, profession, or mindset.

A Deep Dive into TFSAs:

You can avail the following benefits with a self-directed TFSA:

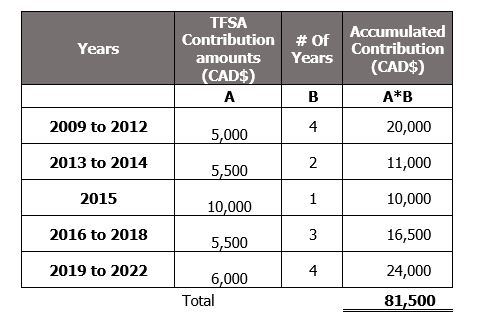

- Yearly contribution limits: An account holder can contribute to TFSA up to the contribution amount set every year. Historically, we have had different contribution amounts as shown below:

- Accumulated contribution: An amazing feature of self-directed TFSAs is that you can use the previous yearly contributions as well. So, if you open an account in 2022, a whopping limit of $81,500 is available at your disposal assuming you have been a legal adult since 2009.

- Unused yearly limit: Do not frustrate yourself if you couldn’t fill up your self-directed TFSA in a year. You can make up the unused limit of a year subsequently in any year as per your financial convenience.

- Tax-free earnings: As the name suggests, all earnings grow and remain tax-free in the TFSA. The interest, dividend, and capital gain you otherwise earn attract taxation. With a self-directed TFSA, all such income is exempt from any kind of taxation. So, it’s a “legal” tax evasion vehicle!

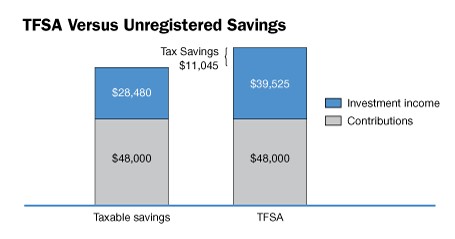

Due to the tax savings, TFSA provides a higher investment income as compared to a regular non-register as shown below:

Source: budget.gc.ca

- Income Splitting: Canadian tax laws blocks attempts to “split” income through transferring income sources to spouse on minor children for tax avoidance. With self-directed TFSA, you can contribute to the spouse’s TFSA as well, and that too with keeping your yearly contribution limit unaffected.

- Earnings increase contribution room: Another brilliant feature is that earnings (interest & dividend) earned within TFSA become a permanent part of the contribution room. In other words, the contribution room is increased from earnings over and above the yearly contribution amount. (We will discuss this more in the “withdrawal” section below.)

- Divorce transfer: A tax-free transfer is made to the spouse as a result of separation. Income afterward is also tax-exempt in the spouse account.

- Death transfer: In the event of death, TFSA can be transferred without any tax consequences to both spouse and non-spouse beneficiaries (i.e., children).

- Non-resident exceptions: If a Canadian resident becomes a non-resident, they are supposed to pay tax on capital gains at the time of becoming a non-resident. This capital gain is calculated through a “deemed” disposal of assets. Luckily, TFSA is one of the exceptions to the deemed disposition rules so there will be zero tax.

Self-Directed TFSA: Things to Watch Out For

Despite numerous benefits, there are certain aspects that you need to be aware of before deciding to open a TFSA to avoid an unpleasant surprise.

- After-tax contributions: Since all earnings and withdrawals attract zero tax, the obvious question arises about the tax status of contributions. These are after-tax so all contributions are not allowed for a tax deduction.

- Excess Contribution: Because you are not paying any tax on earnings within TFSA, common sense dictates that any excess contributions over the allowed yearly limits should be dealt with strictly. This is why a penalty is imposed on over-contribution until the excess is removed from the account or the next year’s contribution amount absorbs it.

- Withdrawal: Although you are allowed to withdraw as much and as many times as you want from the TFSA on a tax-free basis, re-contribution can be only after the completion of the current calendar year. There might be restrictions on withdrawal if you invested in fixed tenure security.

- Interest paid on borrowing: Generally, interest paid on borrowing used directly for a purpose is a deductible tax expense under that income source. For example, interest on a mortgage can be deducted from rental income if borrowings are applied towards a property purchase. You cannot deduct interest paid on a loan taken to make a TFSA contribution.

- Non-spouse transfer: We learned earlier that transfer of TFSA on death is tax-free. Income generation after the transfer is tax-free only for the spouse so for the non-spouse, it will have a tax consequence.

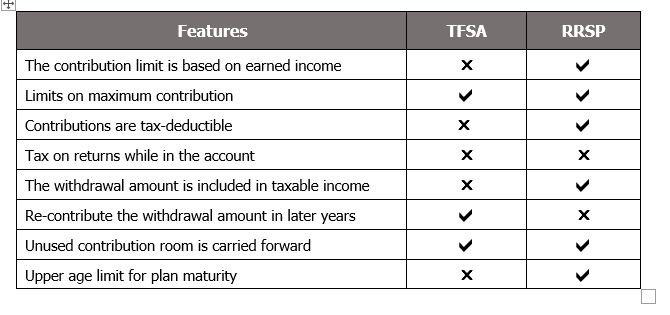

TFSA vs RRSP: Features and Benefits

As a registered account, the TFSA is quite a recent product as compared to the RRSP (Registered Retired Savings Plan), which was introduced in 1957 and is well-known among Canadians. Let’s do a comparison between the two:

How to Open a TFSA:

Opening TFSA is simple, if you meet the criteria just contact the bank representative and they will guide you with the brief process. Some of the banks offering TFSA in Canada are:

- TFSA Scotiabank can be reached at 1.800.4SCOTIA

- TFSA BMO is available at 1-877-225-5266

- TD Direct Investing TFSA is there to help you at 1-888-568-0951

- RBC TFSA can assist you at 1-844-259-1152

- CIBC TFSA can be opened by calling 1-800-465-3863

- HSBC TFSA information is available at 1-888-310-4722

- CanadaLife TFSA details can be accessed here

The above financial institutions are among a few top-notch service providers for self-directed TFSA accounts. For our readers’ convenience, we had put together a review of top-ranked TFSA providers for alternative investors.

If you already have a TFSA and looking for some information on self-directing the existing account to get higher returns, I recommend you go through our page for tips and tricks to manage your account more profitably.

The best time to start investing is now.

Will Your Retirement Weather the Next Financial Crisis?

Gold has been used as an inflation hedge and a way to preserve wealth for millennia. We partnered with Silver Gold Bull, Canada's top-rated gold company (with over 280,000 five-star reviews), to offer Canadians a low-cost and tax-advantaged way to buy gold and silver through an RRSP/TFSA or another retirement plan.

Request More Info

Website: www.SilverGoldBull.ca

Speak to an Expert: (877) 707-4707

About Mustafa Khan

Copyright 2026 Gold RRSP - Helping Canadians invest in physical bullion for retirement