Your Guide to RRSPs in 2026: Canada's Ultimate Retirement Investing Tool

Since RRSPs were introduced in 1957, they’ve become one of the main retirement tools Canadians use to reduce taxes today and build long-term wealth for later. RRSP contributions can lower your taxable income, and your investments can grow tax-deferred until you withdraw (usually in retirement).

Maybe you’re brand new to RRSPs, or maybe you’ve had one for years and want to use it more strategically. Either way, this guide walks you through the essentials, including contribution limits, deadlines, withdrawals, and how RRSPs compare to TFSAs.

What is an RRSP?

An RRSP (Registered Retirement Savings Plan) is a government-registered account that lets you contribute money, potentially deduct those contributions from your taxable income, and invest the assets inside the plan. Investment growth is generally tax-deferred until you withdraw funds.

The history of the RRSP

RRSPs were introduced in 1957 to help Canadians (especially those without employer pensions) save for retirement with a tax incentive.

The pros and cons of RRSP investing

Here’s the honest tradeoff: RRSPs are powerful for tax planning, but you need to understand withdrawals, contribution room, and timing.

👍 Pros

- Tax deduction: contributions can reduce your taxable income (if claimed as a deduction).

- Tax-deferred growth: investments can compound without annual tax drag inside the RRSP.

- Flexible investing: you can often hold GICs, mutual funds, ETFs, bonds, and more (depending on provider/platform).

- Helpful for higher-income years: RRSPs can be especially valuable when you’re in a higher marginal tax bracket.

👎 Cons

- Withdrawals are taxable: RRSP withdrawals are generally added to income in the year you withdraw.

- Withholding tax applies: your institution typically withholds tax at the time of withdrawal (rates vary, including in Quebec).

- You can permanently lose RRSP room when you withdraw (unlike a TFSA, where room can come back the following year).

- Over-contribution penalties: beyond the $2,000 buffer, excess contributions can face a 1% monthly tax.

Your RRSP contribution room (and 2026 limits)

Your RRSP “deduction limit” is based on a CRA formula, but the simple version is:

- Up to 18% of your previous year’s earned income,

- up to the annual RRSP dollar limit, adjusted for things like pension adjustments.

2026 annual RRSP dollar limit: $33,810.

The most reliable place to confirm your personal room is your Notice of Assessment or your CRA My Account, because pension adjustments and past contributions can change the number.

If you’re specifically investing in precious metals inside a registered account, you may also want to read: why add gold to your RRSP and why invest in gold.

RRSP deadlines (and the “first 60 days” rule)

RRSP contributions made in the first 60 days of a calendar year can generally be claimed for the previous tax year (or carried forward, if you choose). CRA posts exact dates each year.

| Item | What it means |

|---|---|

| RRSP deadline for a tax year | Usually the 60th day after year-end (the exact date moves year to year). |

| Example | CRA lists March 2, 2026 as the deadline for contributing for the 2025 tax year. |

How do I open an RRSP?

You can open an RRSP at most Canadian banks, credit unions, brokerages, robo-advisors, and some trust companies. You’ll typically need standard ID and your SIN, and you’ll be asked basic “know your client” questions (risk tolerance, time horizon, investing experience).

If your goal is to hold a broader mix of assets, including gold-related investments, you may prefer a self-directed setup. Here’s our walkthrough: step-by-step guide to setting up a self-directed Gold RRSP.

What can you hold inside an RRSP?

Most RRSPs can hold common assets like GICs, bonds, mutual funds, and ETFs. Self-directed RRSPs at brokerages usually offer the widest menu.

If you’re trying to get gold exposure inside an RRSP, you generally have a few routes:

- Gold ETFs: often the simplest “paper gold” option in a brokerage RRSP (read: how to invest in gold ETFs in Canada).

- Gold mining stocks: higher volatility, company-specific risk.

- Physical bullion via certain structures/providers: depends on the custodian/platform and what they allow.

RRSP withdrawals, withholding tax, and the common “gotchas”

When you withdraw from an RRSP, the amount is generally taxable income in that year. Your financial institution typically withholds tax immediately as a prepayment toward what you’ll owe at filing time.

CRA withholding tax rates (residents of Canada): 10% up to $5,000, 20% for $5,001–$15,000, and 30% over $15,000 (Quebec has different withholding treatment). {index=13}

Also important: if you withdraw RRSP funds “just because,” you usually do not get that contribution room back. That’s one reason many Canadians use TFSAs for short- and medium-term goals, and RRSPs for longer-term retirement planning.

If you want to go deeper on limits, penalties, and over-contribution buffers, see: RRSP contribution limit: what you need to know.

Two special RRSP programs: HBP and LLP

The Home Buyers’ Plan (HBP)

The HBP lets eligible first-time home buyers withdraw RRSP funds to buy or build a qualifying home, then repay the RRSP over time. CRA currently states the HBP withdrawal limit is $60,000, and repayments are generally scheduled over 15 years.

The Lifelong Learning Plan (LLP)

The LLP allows you to withdraw from your RRSP for education or training (for you or your spouse/common-law partner), with an annual withdrawal limit of $10,000 and a total limit of $20,000 per participation. Repayments are generally spread over 10 years.

Choosing between an RRSP and a TFSA

RRSP vs TFSA is one of those questions that sounds simple, but the “best” choice depends on your tax bracket now vs later, your goals, and whether you might need the money before retirement.

| Feature | RRSP | TFSA |

|---|---|---|

| Contributions | May be tax-deductible when claimed | Not tax-deductible |

| Growth | Tax-deferred until withdrawal | Tax-free (growth + withdrawals) |

| Withdrawals | Generally taxable; withholding applies | Generally tax-free; room can return later (rules apply) |

| 2026 dollar limit | Annual RRSP limit: $33,810 (plus personal room calculations) | TFSA dollar limit: $7,000 |

If you want a deeper breakdown (including gold inside each account type), see: TFSA or RRSP: where to put your money (and your gold).

What happens at age 71?

CRA states that December 31 of the year you turn 71 is the last day you can contribute to your own RRSP. After that, you typically convert to a RRIF, buy an annuity, or withdraw the funds (each option has tax implications).

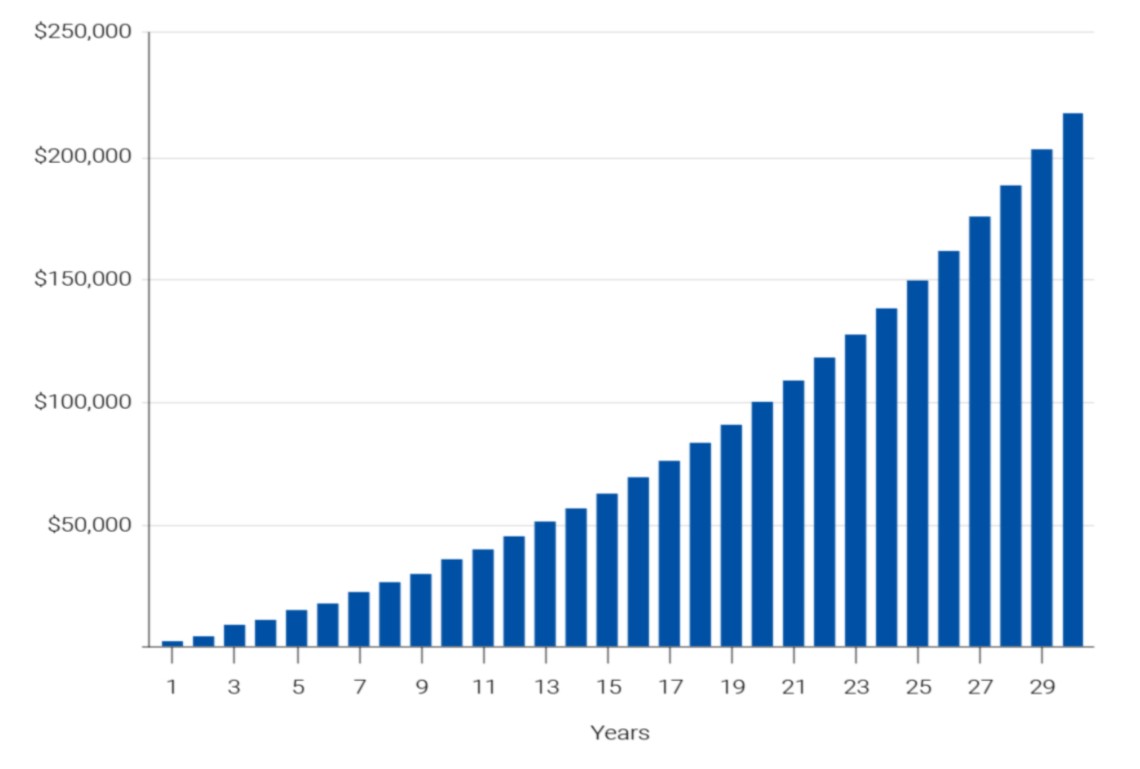

RRSP model portfolios (simple examples)

There’s no universal “best” portfolio, but here are three simple examples many Canadians recognize. Think of these as starting points, not personalized advice.

- Income-focused: more bonds/GICs, lower volatility, lower expected growth.

- Balanced: a mix of stocks and fixed income; some people also add a small allocation to gold/silver for diversification.

- Growth-focused: more equities; higher volatility; typically more suitable with longer time horizons.

Reminder: Investing always involves risk. If you’re unsure, consider speaking with a licensed financial advisor or tax professional.

Figure 1. Source: RBC Royal Bank

RRSP FAQ (2026)

What’s the RRSP contribution deadline?

It’s usually the 60th day after the end of the year. CRA posts the exact date each year (for example, CRA lists March 2, 2026 as the deadline for the 2025 tax year). :

How much can I contribute in 2026?

Your personal limit depends on your earned income, pension adjustments, and past usage. The annual RRSP dollar limit for 2026 is $33,810, but your own room could be lower (or higher if you have carry-forward room).

Is there a penalty for withdrawing from an RRSP early?

There’s typically no special “early withdrawal penalty” like some U.S. accounts, but the withdrawal is generally taxable income and your institution usually withholds tax at the time of withdrawal. You also usually lose that RRSP contribution room permanently.

What are the RRSP withholding tax rates?

CRA lists withholding rates (for residents of Canada) as 10% up to $5,000, 20% for $5,001–$15,000, and 30% over $15,000 (Quebec has different withholding treatment).

How much can I use under the Home Buyers’ Plan?

CRA states you cannot withdraw more than $60,000 in total under the HBP (eligibility rules apply), and repayments are generally spread over 15 years.

How does the Lifelong Learning Plan (LLP) work?

The LLP allows withdrawals of up to $10,000 per year and $20,000 total per participation, with repayments generally required over a 10-year period (rules apply).

What happens if I overcontribute?

CRA explains that you generally pay a 1% per month tax on unused contributions that exceed your RRSP deduction limit by more than $2,000.

When is the last day I can contribute to my RRSP?

CRA states the last day you can contribute to your own RRSP is December 31 of the year you turn 71.

Disclaimer: This guide is for educational purposes and isn’t tax, legal, or investment advice. For personal recommendations, consult a qualified professional.

Will Your Retirement Weather the Next Financial Crisis?

Gold has been used as an inflation hedge and a way to preserve wealth for millennia. We partnered with Silver Gold Bull, Canada's top-rated gold company (with over 280,000 five-star reviews), to offer Canadians a low-cost and tax-advantaged way to buy gold and silver through an RRSP/TFSA or another retirement plan.

Request More Info

Website: www.SilverGoldBull.ca

Speak to an Expert: (877) 707-4707

About Liam Hunt

Copyright 2026 Gold RRSP - Helping Canadians invest in physical bullion for retirement